Cross-border payments alone exceed $190 trillion annually, nearly twice the size of global GDP, and the infrastructure processing most of that volume runs on Java. The language has been the default backend choice in banking and financial services for three decades. Its combination of JVM reliability, strong typing, and mature security tooling matches the needs of transaction systems.

The choice of a fintech Java development company is more consequential than in most other software categories. Compliance architecture, PCI DSS v4.0 scoping, and Spring Boot microservices designed for payment throughput are all expensive decisions to revisit once a platform is in production.

To help you navigate vendor selection, we offer a guide on what distinguishes a Java software company with fintech experience and how to identify the right fit for your specific platform type.

Content:

- Which Java Development Company Is Best for Fintech?

- Who This Guide Is For

- Why Java Remains a Strong Choice for Fintech

- What Qualifies a Java Development Company for Fintech and Banking

- Fintech Specialist vs. General Java Agency

- How We Selected the Best Companies

- Best Java Development Companies for Fintech

- Comparing Java Development Companies

- Java Fintech Engineering Use Cases

- Key Technologies for Java Fintech Platforms

- Security Requirements for Java Banking and Fintech Systems

- Why Kindgeek Is a Strong Java Development Partner for Fintech

Quick Answer: Which Java Development Company Is Best for Fintech?

The best Java development company for a secure banking or fintech platform is not simply the vendor with the largest Java team. The right partner should combine Java and Spring Boot expertise with fintech domain knowledge, payment infrastructure experience, secure API design, DevSecOps, and compliance understanding across PCI DSS, DORA, PSD3, and open banking.

At Kindgeek, that combination is our core practice.

Kindgeek is a fintech-focused Java development partner for companies building secure banking, payment, open banking, digital wallet, and regulated financial platforms. The company combines Java and Spring Boot engineering with fintech domain knowledge, secure API development, compliance-aware architecture, QA automation, DevSecOps, and production support.

Who This Guide Is For

This guide is for CTOs, founders, Heads of Engineering, product leaders, and procurement teams choosing a Java development partner for banking, payments, lending, open banking, neobanking, wealthtech, or regulated fintech platforms.

Why Java Remains a Strong Choice for Banking and Fintech Platforms

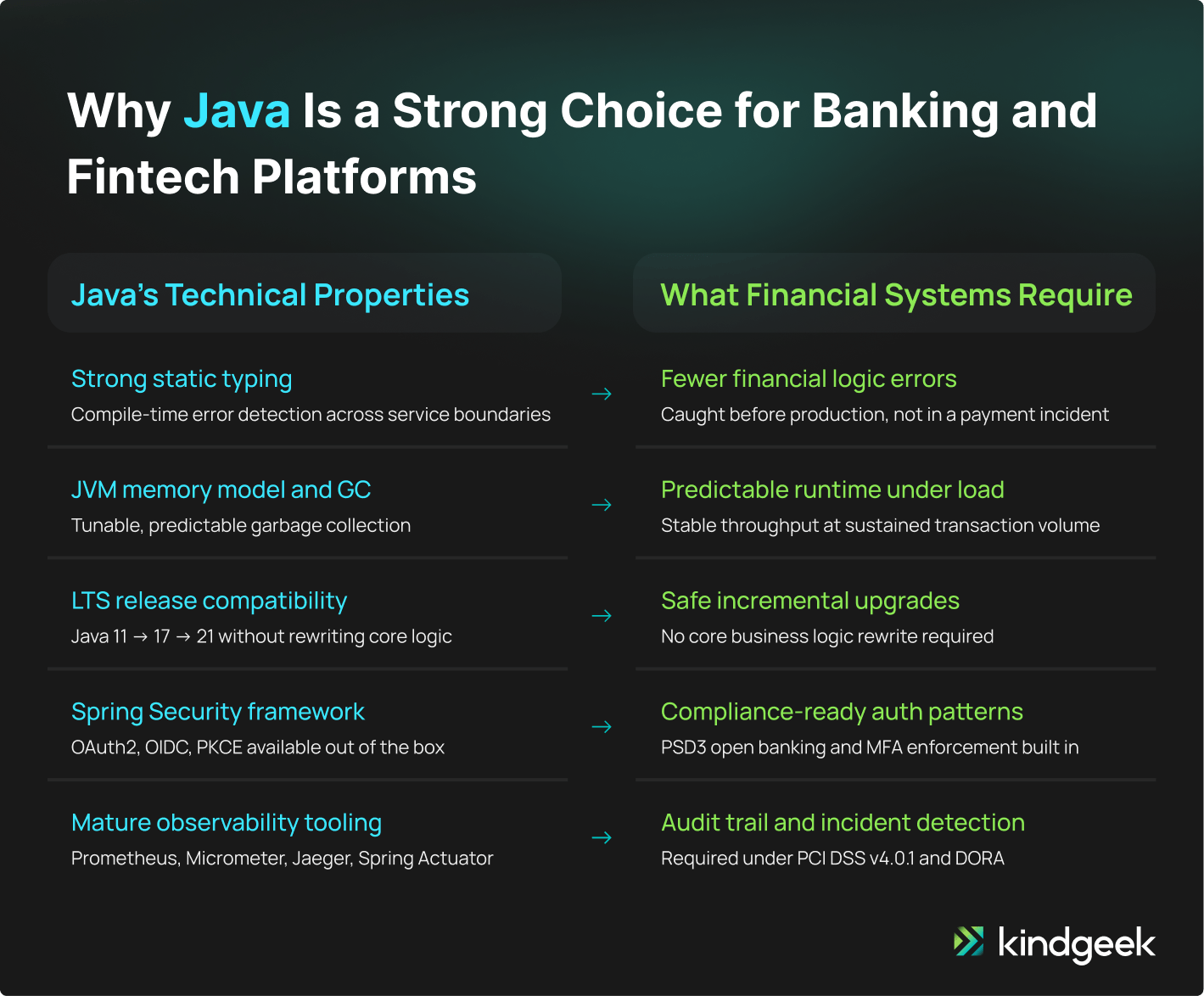

Java has been the dominant backend language in financial services because it reflects concrete technical properties that fit the requirements of transaction processing and regulatory compliance.

Stability, Typing, and the JVM in Financial Systems

Financial platforms require strong typing, deterministic behavior, and deep tooling support for tracing, monitoring, and auditing. Java provides all three. The JVM’s garbage collection, memory model, and decades of profiling tooling make it one of the most operationally predictable runtimes available.

Over 90% of Fortune 500 companies cover their banking software development needs with Java. In fintech, Java is the default for high-throughput payment processing backends where type safety reduces the cost of financial logic errors.

Spring Boot and Fintech Microservices

According to the JetBrains State of Java 2025 report, Spring leads Java frameworks at 65% adoption among professional Java developers. Spring Boot is the practical default for fintech microservices primarily because it simplifies cloud infrastructure migration and offers enterprise-grade security out of the box.

A peer-reviewed study found that combining Spring Cloud components (Service Discovery, API Gateway, Config Server, Circuit Breaker, and Observability) with patterns such as the Saga pattern and CQRS reduces downtime to industry-minimum levels and simplifies adaptation to regulatory changes.

Why Financial Organizations Continue Choosing Java for Mission-Critical Systems

Financial organizations rely on Java for mission-critical systems because its strongly-typed, compiled nature surfaces errors before production. Its legendary backward compatibility allows platforms to safely upgrade runtimes without rewriting core business logic.

Furthermore, the Spring Boot ecosystem provides mature, enterprise-grade integrations for essential infrastructure like Kafka, Redis, and Kubernetes. Fintech teams can deploy secure, distributed payment platforms within a single, cohesive stack.

What Qualifies a Java Development Company for Fintech and Banking

Fintech-specific Java expertise is far less common than general proficiency. The gap shows up directly when building regulated financial software.

Certain capabilities matter more than others when selecting a Java development company for banking and other regulated financial platforms.

Experience with Regulated Financial Products

PCI DSS v4.0.1 is now the active standard. Of the 64 new or updated requirements introduced since v3.2.1, 51 were future-dated and became effective on 31 March 2025. MFA is now required for all access to the Cardholder Data Environment, not just administrator accounts. Continuous risk-based validation has replaced annual checkbox audits.

If you choose a development partner that has not built PCI DSS v4.0-compliant systems in production, you will spend significant onboarding time at the start of the engagement.

DORA became applicable on 17 January 2025 and requires financial entities and their critical ICT providers to formalize ICT risk management, incident reporting, resilience testing, and third-party oversight. Penalties vary by jurisdiction and entity type.

A secure fintech software development company working on EU-facing financial platforms must include ICT risk management frameworks, incident reporting procedures, and third-party oversight in its delivery.

Secure Architecture and API Development

Secure fintech software development means designing systems where authentication, authorization, audit logging, and encryption are architectural concerns. OAuth2, OIDC, PKCE, and role-based access control need to be correctly implemented across all service boundaries. REST APIs need to be designed with OpenAPI specifications and signed at the transport layer.

Payment API integrations introduce further complexity: card scheme certification requirements, 3DS2 strong customer authentication flows, and open banking authorization flows under PSD3 all require specific implementation patterns. Generic Java experience does not transfer here.

Knowledge of Payment Flows and Financial Data

Payment processing involves edge cases like idempotency handling for duplicate transaction prevention, reconciliation logic for settlement discrepancies, partial authorization handling, chargeback workflows, and AML transaction monitoring integration. Expertise in such flows is an essential factor for selecting the best Java development company for a secure banking or fintech platform.

DevSecOps, Cloud Readiness, and Compliance Infrastructure

DORA mandates that regulated financial entities demonstrate digital operational resilience through documented ICT risk frameworks, regular resilience testing, and structured incident reporting. Practically, this requires maintaining CI/CD pipelines with integrated security scanning, container image hardening, infrastructure-as-code with audit trails, and runbooks for incident response.

When evaluating a partner, look for mature DevSecOps practices to avoid compliance debt.

Fintech Specialist vs. General Java Agency

The table below summarizes the key capability differences when evaluating a Java engineering team for secure financial applications against a general agency or freelance arrangement.

| Capability | Fintech Specialist | General Java Agency | Freelance Team |

|---|---|---|---|

| PCI DSS v4.0 architecture | Built-in from day one | Requires external consultant | Unlikely |

| DORA compliance | Integrated into delivery | Post-hoc effort | Not covered |

| Payment integration depth | SEPA, Faster Payments, card schemes | Basic gateway support | Limited |

| Spring Boot microservices | Production-tested patterns | Standard delivery | Variable |

| Regulatory onboarding lag | Minimal | High (2-4 sprints) | High |

| Open banking (PSD3/Open Finance) | Experienced | Partial | Rare |

How We Selected the Best Java Development Companies for Fintech

Each company in this list was evaluated against the following criteria:

Java and Spring Boot Engineering Depth

Production experience with Java 17/21, Spring Boot 3.x, Spring Security, Spring Cloud, and associated infrastructure components.

Fintech and Banking Case Studies

Verifiable delivery of regulated financial products: payment gateways, core banking platforms, card issuing systems, open banking APIs, lending platforms, or digital wallets.

Payment and Open Banking Experience

Direct experience with card scheme integrations, PCI DSS v4.0.1 CDE architecture, 3DS2 authentication flows, and PSD2/PSD3 open banking API implementation.

Security and Compliance Capabilities

Demonstrated approach to PCI DSS scoping, DORA ICT risk management, DevSecOps pipelines with SAST/DAST, and ISO 27001 or SOC 2 certification where applicable.

DevSecOps Maturity

CI/CD pipelines with integrated security scanning, container image hardening, infrastructure-as-code, and documented incident response.

Delivery Model

Full-cycle delivery capacity from discovery through production support, team scalability, and engagement continuity for long-running regulated platform builds.

Verified Reviews and Public Proof

Clutch reviews, client references, awards, and publicly documented case studies.

Best Java Development Companies for Banking and Fintech Platforms

This list focuses on firms with a credible Java-specific track record in financial services. We evaluated Java and Spring Boot engineering depth, fintech domain experience, compliance capability (PCI DSS, DORA, PSD3), delivery model, and verified client outcomes.

1. Kindgeek

Headquarters: Lviv, Ukraine • Founded: 2015 • Team: 200+ engineers

Kindgeek operates exclusively in fintech and has shipped 100+ regulated financial products: PCI DSS-compliant card issuing systems, EMI-licensed neobank infrastructure, open banking integrations, and payment processing platforms.

70% of clients come from referrals, and average engagement exceeds two years. If you’re looking for a partner who can build a secure fintech platform in Java, Kindgeek is well-positioned to support both growth and compliance.

Best fit for: European fintech startups and scale-ups needing a long-term engineering partner with compliance-first Java delivery.

2. EPAM Systems

Headquarters: Newtown, Pennsylvania, USA • Founded: 1993 • Team: 60,000+ globally

EPAM is one of the largest engineering services firms with a dedicated financial services practice covering fraud detection, wealth management, core banking modernization, and payment systems. Their Java engineering capability is mature, with deep experience in large enterprise banking transformations.

Best fit for: large enterprise banks and financial institutions requiring a global delivery model at scale.

3. Intellias

Headquarters: Chicago, USA • Founded: 2002 • Team: 3,000+

Intellias has a dedicated financial services practice covering digital banking platform development, PSD2/PSD3 open banking API design, RegTech and KYC/AML integrations, and AI-powered analytics for financial institutions. Their Java and Spring Boot work is well-documented across core banking and neobank engagements.

Best fit for: mid-market to enterprise financial institutions and fintechs in Europe building or modernizing digital banking infrastructure.

4. ScienceSoft

Headquarters: McKinney, Texas, USA • Founded: 1989 • Team: 750+ engineers

ScienceSoft has a dedicated financial services practice covering banking software, payment gateways, investment platforms, and lending solutions. Their Java track record includes a PA-DSS compliant payment gateway with 3D Secure authentication, a BNPL platform, and a trading automation system built for NASDAQ and NYSE.

Best fit for: financial institutions and fintechs requiring a large, ISO-certified Java team with a verifiable payment gateway and regulated product delivery across banking, lending, and investment verticals.

5. DataArt

Headquarters: New York, USA • Founded: 1997 • Team: 5,000+

DataArt is a global technology consultancy with over two decades of fintech experience. Their financial services work covers core banking software, trading platforms, investment management systems, and payment infrastructure for banks and financial enterprises. Java is a primary backend language in their financial services stack.

Best fit for: established financial institutions and capital markets firms needing a consultancy with enterprise fintech depth.

6. N-iX

Headquarters: Plantation, Florida, USA • Founded: 2002 • Team: 2,400+

N-iX has a dedicated financial services practice with delivered finance projects and engineers with financial services domain knowledge. Their banking work covers neobank transformation, cloud-based payments platforms, KYC/AML systems, and core banking re-platforming. N-iX holds FSQS certification, PCI DSS compliance (v3.2.1), ISO 9001, and ISO 27001, and has passed CyberGRX risk assessment.

Best fit for: banks, PSPs, and fintech companies in Europe and North America requiring a mid-to-large engineering partner with verified compliance certifications and a strong track record in core banking modernization and payment platform development.

7. Itexus

Headquarters: United States (development offices in Europe) • Founded: 2013 • Team: 160+

Itexus focuses exclusively on financial software, covering digital banking, trading platforms, investment management, crypto, and insurance. Their delivery covers full-cycle development from architecture through deployment, with compliance built to SOC 2, PCI DSS, and ISO 27001 standards. Java features prominently in their backend stack alongside .NET, used for microservice architectures and high-load financial platforms.

Best fit for: North American and European fintechs and financial institutions needing a specialist team with a strong compliance engineering track record across banking, trading, and investment platforms.

8. SDK.finance

Headquarters: Vilnius, Lithuania • Founded: 2013 • Team: 200+

SDK.finance is a white-label fintech platform provider that sells a modular source-code platform for digital banks, wallets, and payment systems, alongside custom development services. Their platform supports digital wallets, mobile banking, payment applications, and money transfer products. It is built to accelerate time-to-market by providing pre-certified financial modules rather than building from scratch.

Best fit for: fintechs and banks that want to launch faster using a white-label fintech platform with source code access, with custom Java development layered on top where required.

9. Code & Pepper

Headquarters: Suwałki, Poland • Founded: 2006 • Team: 70+ engineers

Code & Pepper is a fintech-specialist software development firm building financial products across digital banking, open banking, lending, payment solutions, and wealthtech. Their Java developer practice is explicitly positioned for fintech, with backend development, API development, and DevOps services tailored to financial services clients. Verified fintech work includes payment, lending, and open banking platform development.

Best fit for: fintech startups and growth-stage companies needing a focused, senior-heavy Java and fintech team for product builds across banking, lending, payments, and open banking.

10. Unosquare

Headquarters: Portland, Oregon, USA • Founded: 2009 • Team: 1000+

Unosquare provides Java development services for fintech, covering high-frequency trading platforms, secure payment gateways, fraud detection engines, core banking modernization, and risk modeling software. Their Java fintech stack includes Spring Boot for microservices, Apache Kafka for real-time transaction feeds, jPOS for ISO-8583 financial transaction standards, and Keycloak for identity management. They build to PCI-DSS and SOC2 standards and report 98% client retention.

Best fit for: North American fintechs and financial institutions requiring nearshore Java teams with specific fintech tooling knowledge (jPOS, ISO-8583) and US time zone alignment.

Comparing Java Development Companies for Fintech Projects

Let’s map the top 10 companies to the most common selection criteria: project type, company stage, and financial vertical.

Best Fit by Project Type

| Project Type | Best-Fit Companies | Key Reason |

|---|---|---|

| New fintech product (greenfield) | Kindgeek, Code & Pepper, Unosquare | Full-cycle delivery, compliance-first architecture from sprint one |

| Core banking modernization | EPAM, Intellias, N-iX | Enterprise-scale delivery, legacy migration experience, verified banking clients |

| Payment gateway / PSP | Kindgeek, Itexus, ScienceSoft | PCI DSS architecture depth, verified payment gateway case studies |

| White-label platform launch | SDK.finance, Kindgeek | Pre-built fintech platform components, source-code access |

| Open banking / API platform | Intellias, Kindgeek, Code & Pepper | PSD2/PSD3 implementation, OAuth2 authorization server experience |

| Lending or credit platform | Kindgeek, Unosquare, Itexus | Origination workflow, Kafka-based loan lifecycle, credit directive compliance |

Best Fit for Startups vs. Enterprises

| Stage | Recommended Companies | What to Prioritize |

|---|---|---|

| Early-stage startup | Kindgeek, Code & Pepper, SDK.finance | Speed to market, white-label options, senior-heavy small team, compliance from day one |

| Growth-stage / Series A–B | Kindgeek, Intellias, N-iX | Scalable team model, DevSecOps maturity, increasing regulatory complexity |

| Enterprise / large institution | EPAM, ScienceSoft, DataArt | Global delivery capacity, ISO certifications, large parallel workstreams |

| Platform-as-a-service fintech | SDK.finance, Itexus, Unosquare | Multi-tenant architecture, API marketplace design, flexible engagement models |

Best Fit by Financial Vertical

| Vertical | Recommended Companies | Relevant Capabilities |

|---|---|---|

| Digital banking / neobank | Kindgeek, Intellias, SDK.finance | EMI licensing support, core banking microservices, PSD3 open banking APIs, card issuing |

| Payments & payment gateways | Kindgeek, ScienceSoft, EPAM | PCI DSS v4.0.1 CDE architecture, card scheme integration, 3DS2, verified payment gateway delivery |

| Lending & credit | Kindgeek, Unosquare, N-iX | Origination workflow, Kafka-based loan lifecycle management, AML/KYC integration |

| Digital wallets & e-money | Kindgeek, SDK.finance, Code & Pepper | EMI compliance, multi-currency wallet architecture, open banking payment initiation |

| Wealth management / investment | DataArt, ScienceSoft, EPAM | Trading platform engineering, portfolio management, financial data analytics, MiFID II compliance |

Java Fintech Engineering Use Cases

Digital Banking Platforms

Core banking platforms require high transaction throughput, strong consistency guarantees, multi-currency account management, and integration with multiple payment rails. A company experienced in Spring Boot fintech platforms can handle these requirements well.

Payment Platforms and Payment Gateways

Payment gateway development requires deep integration with card schemes (Visa, Mastercard), acquiring banks, and alternative payment methods, alongside PCI DSS v4.0 architecture and 3DS2 authentication flows. Java’s reliability under high transaction volumes and Spring Boot’s ecosystem support for the relevant integrations make it the standard choice.

That’s why scheme integration experience is required when choosing a Java development partner for payment platforms.

Lending and Credit Platforms

Credit scoring engine integration, origination workflow management, loan servicing logic, and regulatory reporting for consumer credit directions are all necessary for lending platforms. Kafka-based event-driven systems are good for managing the state machine complexity of loan lifecycle management and preserving auditability. Virtual threads in Java 21 can enhance multi-step origination flows’ responsiveness without necessitating reactive programming redesign.

Open Banking and API Platforms

PSD3 bolsters PSD2’s open banking platform with API performance, availability, and third-party provider access management standards. Developing Open Finance API platforms in Java involves OAuth2 authorisation servers, developer portals, rate limiting, and SLA monitoring.

Key Technologies for Java Fintech Platforms

Core Backend Stack

- Java 21 / 25 (LTS): Virtual threads (Project Loom) for high-throughput, I/O-heavy payment processing without the code complexity of reactive programming rewrites.

- Spring Boot 4.x: Microservices foundation featuring native gRPC integration, embedded servers, and production-ready metrics via Actuator.

- Spring Security: Robust OAuth2, OIDC, PKCE, and method-level authorization enforced across all microservice boundaries.

- Spring Cloud: Resilient service mesh architecture managing service discovery, API routing, circuit breaking, and centralized configuration.

- Hibernate/JPA: Transactional data access with native audit event listener support for historical tracking.

API Design and Authentication

- OpenAPI 3.1 / 3.2 Specifications: Standardized schema documentation with native support for streaming/Server-Sent Events (SSE) for real-time transaction tracking.

- OAuth2 Authorization Servers: Securing Open Banking and Third-Party Provider (TPP) access in alignment with Financial-grade API (FAPI) standards.

- API Gateways (Spring Cloud Gateway, Kong): Enterprise edge layers handling strict rate limiting, token introspection, and localized PCI DSS audit logging.

Event Streaming and Data

- Apache Kafka: High-throughput transaction streams, durable write-ahead audit logs, and decoupling via CQRS and Event Sourcing patterns.

- PostgreSQL: Relational database engine for core transactional accounting data requiring strict ACID guarantees.

- Redis: High-performance in-memory layer for distributed session management, token caching, and localized rate limiting.

- Elasticsearch / OpenSearch: Distributed search indexing optimized for multi-field transaction lookups and real-time AML (Anti-Money Laundering) monitoring.

Infrastructure and Observability

- Kubernetes with Helm: Orchestration layer managing containerized microservice deployments, auto-scaling, and rolling updates.

- Docker / Container Runtimes: Base container images hardened and stripped to minimal runtimes in compliance with CIS benchmarks.

- Terraform / OpenTofu: Infrastructure-as-Code (IaC) configuration management maintaining verifiable cloud architecture audit trails.

- OpenTelemetry (Prometheus, Grafana, Jaeger): Unified telemetry standard for distributed tracing, log aggregation, and real-time service health dashboards.

Security Requirements for Java Banking and Fintech Systems

Authentication, Authorization, and Access Control

- Multi-Factor Authentication (MFA): Strictly required for all internal, administrative, and standard access to the Cardholder Data Environment (CDE) under PCI DSS v4.0.1 mandates.

- Zero-Trust Boundary Control: Role-Based Access Control (RBAC) enforced at the API gateway and network mesh layer, preventing lateral movement inside internal networks.

- Secure Token Lifecycle: Cryptographically signed JWT tokens featuring short time-to-live (TTL), automated rotation, and stateless revocation tracking.

- Method-Level Authorization: Pervasive use of Spring Security’s @PreAuthorize annotation across all microservice endpoints for granular, role-level backend protection.

API Security and Data Encryption

- Transport Layer Security (TLS 1.3): Mandatory encryption in transit for all internal and external API communications, with legacy protocols (TLS 1.2 and below) explicitly disabled.

- Field-Level Encryption (FLE): Explicit application-layer encryption for high-risk sensitive elements (e.g., PANs, account numbers, and PII) prior to database persistence.

- Encryption at Rest: Full-disk or database-level AES-256 encryption within all data stores holding cardholder information.

- Hardware Security Modules (HSM): Cloud-native or physical HSM integration for secure cryptographic key management conforming to NIST SP 800-57 guidelines.

Audit Logs, Traceability, and Fraud Prevention

- Immutable Audit Logging: Read-only, append-only logs tracking all payment data access, administrative shifts, and infrastructure configuration to meet DORA and PCI DSS compliance.

- Cryptographic Log Integrity: Cryptographic hashing or sequential signing of transaction logs to immediately flag and isolate tampering attempts.

- Real-Time Fraud Scoring: Stream processing over Apache Kafka for inline fraud evaluation, coupled with persistent decision logging for dispute resolution.

DevSecOps and Secure Release Processes

- Static Application Security Testing (SAST): Automated code analysis pipelines utilizing tools like SonarQube or Checkmarx to block application vulnerabilities pre-merge.

- Dynamic Application Security Testing (DAST): Automated run-time vulnerability testing actively executed against isolated staging environments.

- Software Bill of Materials (SBOM) & Dependency Scanning: Continuous security monitoring of open-source libraries via OWASP Dependency-Check or Snyk to prevent supply-chain attacks.

- Container Image Scanning: Native image scanning using Trivy inside the CI/CD pipeline to flag and mitigate OS-level vulnerabilities before cluster deployment.

Why Kindgeek Is a Strong Java Development Partner for Fintech

The best Java development company for banking platforms understands both enterprise-grade software engineering and the realities of financial regulation.

Kindgeek focuses exclusively on fintech, giving clients direct experience with the compliance architecture, payment integrations, and regulatory constraints.

Our engagements cover:

This matters for regulated platforms where the partner relationship extends beyond launch.

Looking for a technology partner for a Java-based banking platform?

We support the delivery of compliant systems across digital banking, card issuing, payment processing, and open banking. Fully aligned with PCI DSS v4.0, DORA, and PSD3. Let’s talk about your project.

Contact usHow much does Java fintech development cost?

Cost depends on platform complexity, compliance scope, and team structure. A minimum viable payment gateway with PCI DSS compliance and one or two payment method integrations typically requires 6-12 months of engineering work with a team of 5-10 engineers. A full core banking platform or neobank infrastructure with card issuing, open banking, and multi-currency support requires 12-24 months with a larger team.

What security and compliance experience should a Java fintech partner have?

A Java development partner for a regulated fintech platform should demonstrate: experience scoping and building PCI DSS v4.0.1-compliant Cardholder Data Environments, familiarity with DORA ICT risk management requirements (applicable from January 2025), working knowledge of PSD2/PSD3 open banking authorization flows, CI/CD pipelines with integrated SAST and DAST scanning, and ISO 27001 or SOC 2 certification.

How do I choose a Java vendor for a payment platform?

When looking for the best vendor for Java banking software development evaluate fintech domain knowledge first, Java seniority second. Ask for specific examples of PCI DSS v4.0 compliance work, open banking API implementations, and payment scheme integrations. Assess their DevSecOps maturity: CI/CD pipelines, security scanning, container hardening, and incident response documentation. Start with a discovery or technical audit engagement before committing to full development. This reveals both their technical capability and their working style.

Which company is best for Java fintech development?

The best Java development company for fintech is one that combines strong Spring Boot and Java engineering with direct experience building regulated financial products.

Why is Spring Boot popular in fintech platforms?

Spring Boot is the dominant Java framework in fintech because it significantly reduces the configuration overhead of building production-ready microservices. Its built-in support for Spring Security (OAuth2, OIDC, PKCE, role-based access control), Spring Cloud (service discovery, API gateway, circuit breaker), and Spring Actuator (health monitoring, metrics) maps directly to what payment and banking platforms require.

Is Java good for fintech and banking software development?

Yes. Java offers robust typing, JVM reliability, sophisticated security frameworks, and a rich production tools ecosystem for banking systems. Backward compatibility allows long-lived payment platforms to be maintained and improved incrementally, which is important for regulated systems with tight change management requirements. Along with a well-tested runtime, Spring Boot and Spring Security bring compliance-relevant features like role-based access control, OAuth2 integration, and full audit logging.

Which Java development companies build secure banking platforms?

Companies with verified delivery of regulated banking products include Kindgeek, EPAM, Intellias, N-iX, ScienceSoft, and DataArt. The key differentiators are compliance certification (PCI DSS, ISO 27001, FSQS), verifiable case studies for payment gateways or core banking systems, and demonstrated DevSecOps maturity.